How banks can support mortgage customers to reduce their carbon emissions

Mon, 31st Mar 2025

The global mortgage market is huge and the homes we live in are big contributors to carbon emissions. Banks have the data, tools and influence needed to reduce financed emissions and drive meaningful change. Keep reading to find out how…

What's the size of the problem?

The global mortgage lending market was valued at approximately $11.5 trillion in 2021 and is projected to reach over $27.5 trillion by 2031, growing at a compound annual growth rate of 9.8%.

This vast market is associated with a substantial carbon footprint—primarily linked to the energy used to heat, cool and power each home that has a mortgage. In the United States alone residential properties account for about 954 million tons of CO₂ equivalent annually. This is equivalent to driving around the earth 81 million times! Agency residential mortgage-backed securities (RMBS) finance approximately 17% of these emissions, equating to around 160 million tons of CO₂ equivalent each year showing up on banks' carbon accounts.

What's more, financed emissions (which include emissions from loans and investments) represent around 75% of a bank's total carbon footprint. This demonstrates the significant impact of lending activities, including mortgages, on overall emissions.

The challenge: measuring and managing carbon emission

Regulators globally are ramping up requirements around disclosing emissions with greater accuracy.

Building on the good reporting and disclosure work banks are already doing, banks are now partnering with Cogo to enhance how they support customers to potentially save money and help reduce their household emissions.

The real challenge lies in aligning measurement with helping customers to take action to reduce their household emissions. Doing so doesn't just align with banks' reporting needs; it also helps deliver real business benefits. Enabling customers to explore low carbon home energy solutions and sustainable financing options encourages them to invest in improvements to their properties that will potentially save them money.

A smarter, mortgage market

Imagine a world where a homeowner considering an upgrade — like installing solar panels or better insulation — could access tailored recommendations through their bank, including financing options to support those upgrades. Instead of struggling with upfront costs, they could access sustainable finance options, benefit from potentially reduced energy bills and help reduce their carbon footprint. Meanwhile, their bank can better support their customers in facilitating this upgrade, which has not only helped reduce its financed emissions and potentially strengthened customer loyalty, but also expanded its sustainable lending portfolio.

Combining measurement with active impact

Banks don't have to start from scratch to drive this kind of change. Cogo's Home Energy product is a ready-to-implement solution that empowers customers to make energy-efficient choices while unlocking new commercial opportunities and boosting regulatory compliance.

By combining user input with real home energy data, Cogo's solution enables homeowners to:

-

Understand their home's carbon footprint

-

Compare their current energy consumption with potential upgrade scenarios

-

Receive tailored recommendations for solutions like solar panels or insulation

-

Get estimates on energy savings, costs and payback periods

Through this proactive approach, banks can connect customers with trusted suppliers and financing options, making home energy upgrades more accessible and achievable.

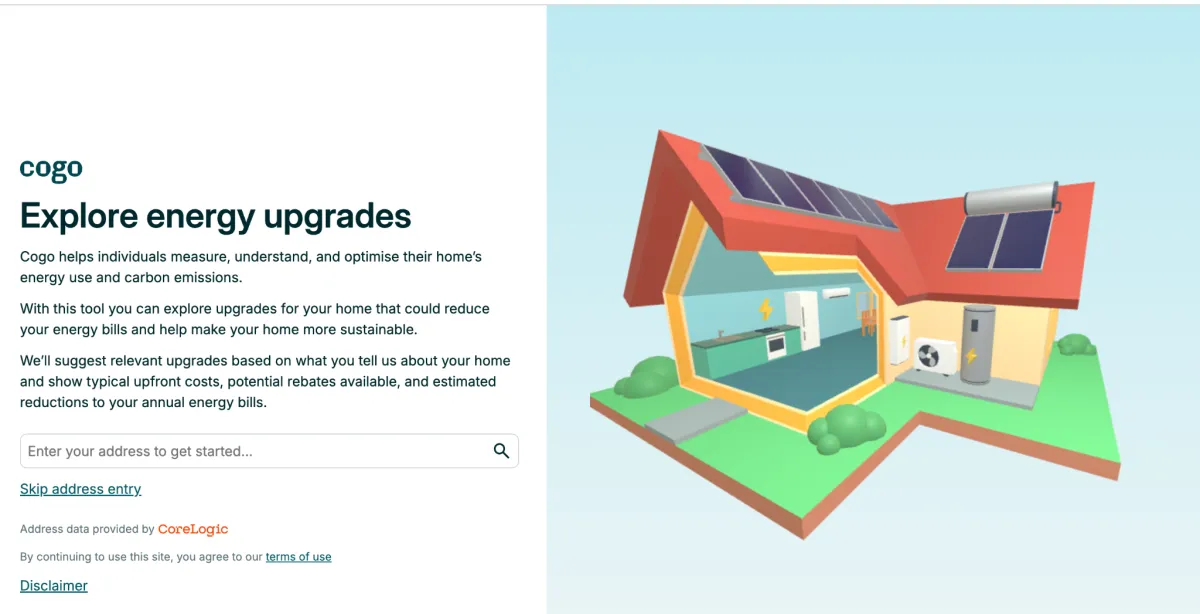

Fig 1. Cogo's Home Energy tool on the Westpac website.

Real impact: Westpac leading the way

Westpac (Australia) has already embarked on a pilot with Cogo to launch a home energy tool which helps their home loan customers identify and implement energy upgrades. Through a quick online assessment, customers receive personalised recommendations, estimated costs, potential energy savings and information on available rebates. This kind of engagement helps banks to better support its customers with their home energy transition .

This engagement helps banks support customers in their home energy transition whilst supporting progress on their own sustainability targets.

The opportunity is clear

Banks are at a critical junction and now is the time to find greater opportunities to help customers reduce emissions. This will help position banks to lead in the sustainability space as they aim to strengthen customer trust, create new lending opportunities and de-risk mortgage portfolios.

Broad engagement of mortgage holders isn't just an ideal - it's an achievable goal with the right technology. With Cogo's solutions, the transition from measurement to impact can be seamless.

The question isn't whether banks should act - but how quickly they will.

Interested in learning how Cogo can help your financial institution drive the home energy transition? Get in touch with our team today.